Defined Cost Verification at Crossrail

Document

type: Micro-report

Author:

Ian Fowkes

Publication

Date: 09/07/2018

-

Read the full document

Introduction and Industry Context

Large complex infrastructure projects funded or part-funded by public funds commonly utilise the NEC[1] Option C form of contract. The Option C contract is a target cost (shared risk) contract that relies on a fully transparent approach from the supply chain.

Both cost and change adjustment are subject to contemporaneous scrutiny in accordance with both Main Contract and Works Information provisions.

To further enhance the `open book` philosophy and to aid transparency with respect to the Fair Payment Charter[2] the Crossrail Contracts also prescribed the use of a Project Bank Account (PBA) . Transactions within the PBA form the parameters of Cost Verification activity.

It is imperative that a Programme with the magnitude and complexity of Crossrail adopts a coherent, contemporaneous, consistent and collaborative approach to the verification of Defined Cost.

Crossrail defined its Cost verification policy and procedure from the outset, but during the course of the project also developed a framework and guide to ensure consistent application by the cost verification team.

This paper outlines the Crossrail approach to the verification of Defined Cost throughout the duration of the programme. Throughout the body of the report key themes repeat:• Early engagement / collaboration

• Promotion of cost management

• Expectation management

• Contemporaneous communication of findings

• Consistency of recommendations

• Availability of evidential documentation ( Future Audit Proofing)The approach has been informed by the experience of implementing Cost Verification Activities on other large scale Infrastructure Programmes.

Start Up

Structure and reporting lines are a key consideration when developing both a Cost Verification (CV) function and its link to a commercial strategy.

The Cost Verification (CV) function is quasi-independent in that it supports the Project Manager in their contractual obligations, but has a direct reporting line to the Commercial directorate. This enables findings and recommendations to be applied in a timely and consistent way across the programme and support commercial strategy with respect to both outcome and governance.

The formation of the CV function is critical. Ideally it should include individuals from multi discipline backgrounds. The Crossrail CV function includes individuals with financial, accountancy, contract delivery (equipment), commercial and internal audit backgrounds. A number of team members also have previous cost verification experience on large infrastructure programmes such as HS1, Heathrow T5, and London 2012.

It is important that key individuals within the CV function have the experience and ability to work within the emotive area of Not Defined and Disallowed Cost because it ultimately impacts on the Contractor`s bottom line.

The size of the CV function is ultimately driven by the approach or extent to which Defined Cost will be reviewed.

It is impossible to verify all incurred Defined Cost on a programme of Crossrail`s magnitude, circa £6.5b of Defined cost, 62% of which is covered by the main contract Schedule of Cost Components (SoCC). The CV function therefore had to adopt a risk based approach

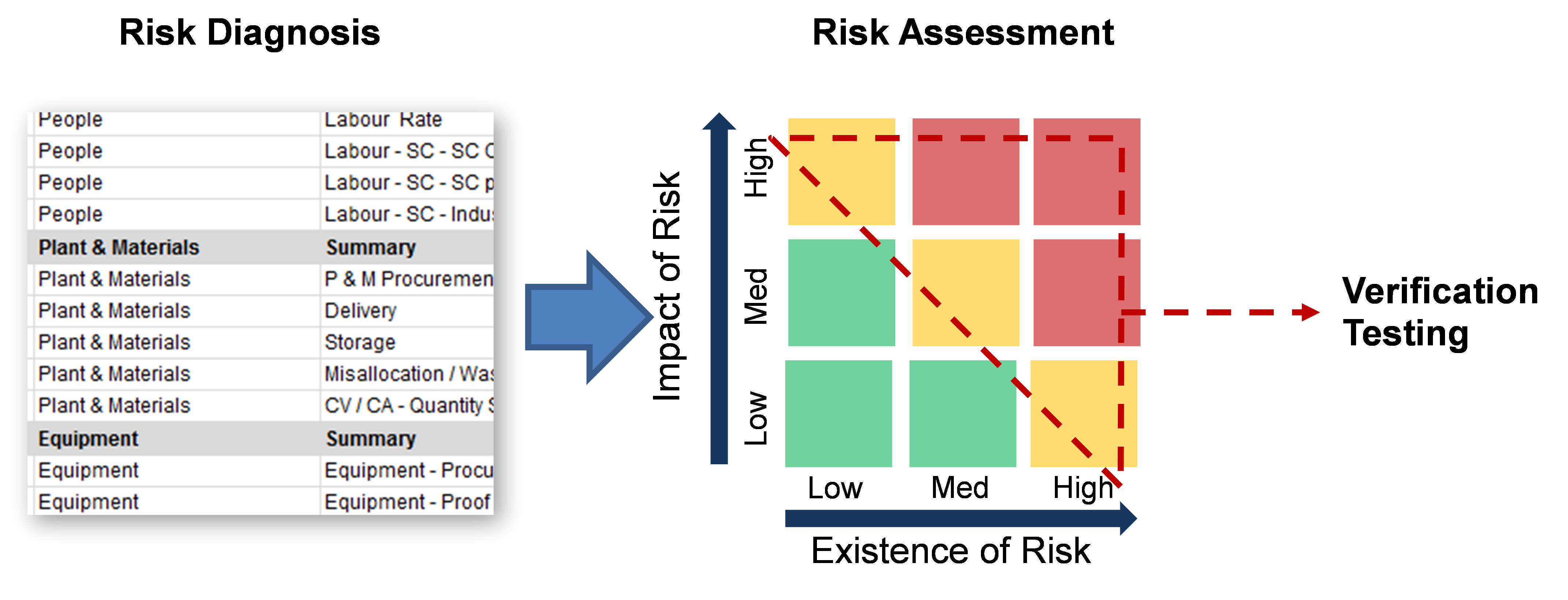

The risk based approach fundamentally breaks down Defined Cost elements by cost component as stipulated in the Main Contract Schedule of Cost Components, and by the associated drivers of cost (processes). A framework document was developed for each live Crossrail NEC option C contract.

The depth into which the risks are tested depends on the risk attributed to each element of the framework. Where a low level of risk is identified, testing will be limited whereas high risk areas will be tested in detail.

The applied `judgement of risk` assessment also benefits from the experience of CV function. Figure 1 below shows a typical risk assessment is carried out on each element.

Figure 1 – Typical Risk Assessment Analysis

The development of a Framework enables the production of coherent reports detailing cost verification coverage by both Defined Cost element and by contract.

Monthly dashboards, driven by the Framework, enable the CV function to identify trends, target incomplete areas and compare Tier 1 Contractor performance.

The Crossrail CV function ethos also demands early engagement with Tier 1 site staff to establish working relationships and to promote a collaborative approach. Having this approach from the CV function ensures early `expectation management` within the supply chain.

Examples of early activity include:• New contracts questionnaire meetings

• Collaboration in Tier 1 Contractor`s “Accounts and Administration Plan” presentation

• Early reviews on high risk and high impact cost elementsConcurrency of Programme

Throughout the duration of the programme, CV function reviews are carried out, they are dynamic in nature, relevant to conditions of contract and works information requirements.

It was a conscious decision not to draft lengthy audit type reports where pertinent points may sometimes get lost.

All CV function reviews carried out on behalf of the relevant Project Manager are communicated under the agreed contract mechanisms.

CV function reviews typically recommend:• Not Defined Cost

• Potential Disallowed Cost ( typically Defined Costs not support by accounts or records)

• Lack of process or process non-complianceReview recommendations are administered by the Project Manager`s commercial team and tracked by the CV function.

All CV function recommendations and actions are monitored via a bespoke CV action tracker document. This document, maintained by the CV function, is the key to demonstrating an evidence based Defined Cost verification process to any future stakeholder, third party or Government body audit.Close Out

From a commercial perspective, the timely settlement of Contracts, with minimal disputes, is considered a success as it is the optimal use of time and resource.

The CV process and associated documents provide `real time` reports on both SoCC coverage and identifies outstanding actions detailed by contract.

This information can be used for progressive agreement of Defined Cost by way of an Employers Supplemental Agreement or ultimately Settlement Agreement (these items are detailed in the Commercial Strategy Learning Legacy paper).

Supplemental Agreements, instigated by the employer and supported by CV activity, provide an element of certainty for both Contractor and Employer with respect to Defined Cost.

The CV function produces a status report at the time of final assessment. This document ties together all activity throughout the contract period in a format that enables future potential auditors to drill down to all specific reviews / recommendations and any associated working papers.Added Value

CV activity is not confined to Contract reviews, examples of added value include:

• Interrogation of Bottom Up Forecast (BUF) Rates

• Co-ordination of Asset management / disposal within the supply chain.

• Risking future cost from a Not Defined / Disallowed cost perspective

• Benchmarking of equipment / labour rates

• Peer review of Tier 1 management of back- to- back contracts – Option C,E

• Active participants in the Fraud Risk Assurance Group (FRAG)This further demonstrates the benefits of having a dedicated CV function.

Lessons Learned

It is beneficial to have early engagement of CV professionals – who have direct input into Works Information and /or modifications to the main Contract Schedule of Cost Components.

Consistent and contemporaneous review is essential for the management of expectation within the supply chain.

A collaborative relationship with Tier 1 contractors, together with the promotion and sharing of best practice can be as powerful as any of the other remedies available under contract, with respect to impact on outturn Defined Cost

Continuous engagement with Commercial Teams and Tier 1 contractors is essential to ensure actions and recommendations are applied in a timely and consistent manner.

Recommendations for Future Projects

• The early engagement of CV professionals, ideally in-house and reporting through the Commercial Directorate.

• The use of Project Bank Accounts (PBA) is recommended for major projects with a main contract and subcontract procurement structure. Further, the new NEC 4 contract defines timescales by which the Project Manager is to complete the review of Defined Cost, which will make the visibility provided by a PBA even more necessary.

References

[1] New Engineering Contracts (NEC) – [online], available at:

https://www.neccontract.com/About-NEC/History-Of-NEC . Accessed 5 June 2018.

[Related Link – NEC Crossrail case study – [online] available at:

https://www.neccontract.com/NEC-in-Action/Case-Studies/Crossrail]. Accessed 5 June 2018.[2] Government Policy Paper, Department for Business, Energy and Industrial Strategy, 10 August 2016; “Construction supply chain payment charter” [online], available at https://www.gov.uk/government/publications/construction-supply-chain-payment-charter . Accessed 5 June 2018.

-

Document Links

-

Authors

Ian Fowkes - Crossrail Ltd

As Crossrail`s Defined Cost Verification Manager Ian has been responsible for development and implementation of Crossrail’s Defined Cost Verification processes and ethos. Ian`s career has seen him involved in the development of Cost Verification activity over a period of 18 years, latterly as head of Cost Verification on HS1 and London 2012. Ian’s career in infrastructure spans 38 years, previously working for Tarmac Construction, Bechtel, and Laing O`Rourke.